904-850-8900

Direct to Jerel (Owner)

The clock is real, but you likely have more time than it feels like. Get three written options — cash price, a higher-price monthly plan, and an honest comparison to listing — before you decide anything.

Serving Jacksonville + surrounding areas — Fernandina, Yulee, Orange Park, St. Augustine, Palatka, and nearby.A homeowner was behind on payments and upside down, with a code lien on top. We took over her existing mortgage dollar-for-dollar and covered closing costs — she brought $0 to closing.

Each card shows a real situation we solved — with a redacted closing statement you can review. Look for "Due to Seller" on the HUD.

📁 Full redacted closing statements available on request. Three of these closed through a Florida real estate attorney; the seller-financed purchase closed directly between the two parties.

The questions we hear most from sellers in your situation.

⚠️ Doing nothing is the most expensive option here.

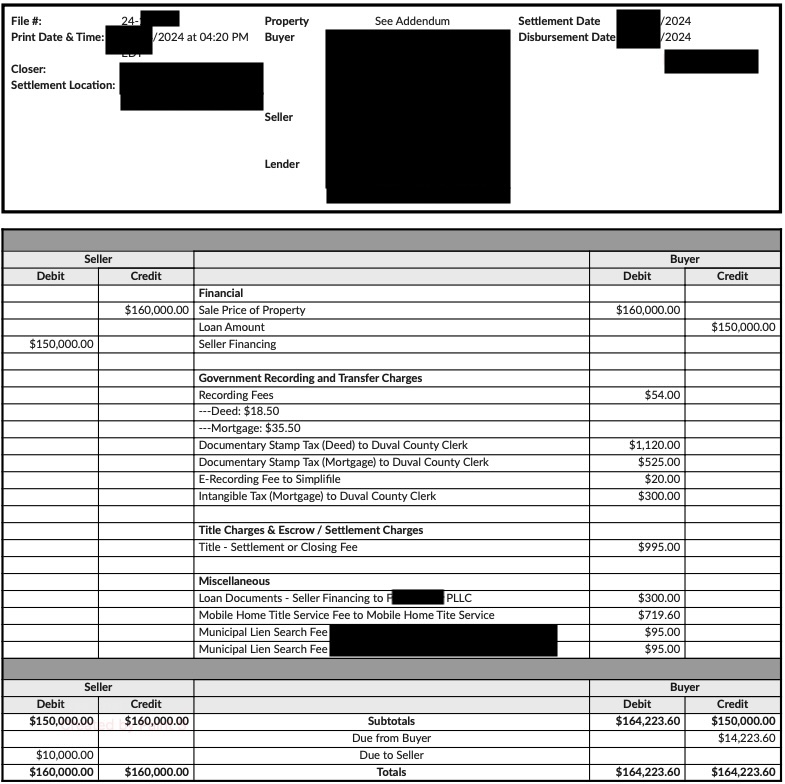

Personal information redacted. Sale price: $160,000. Seller financing: $150,000. Attorney-closed, Duval County, 2024.

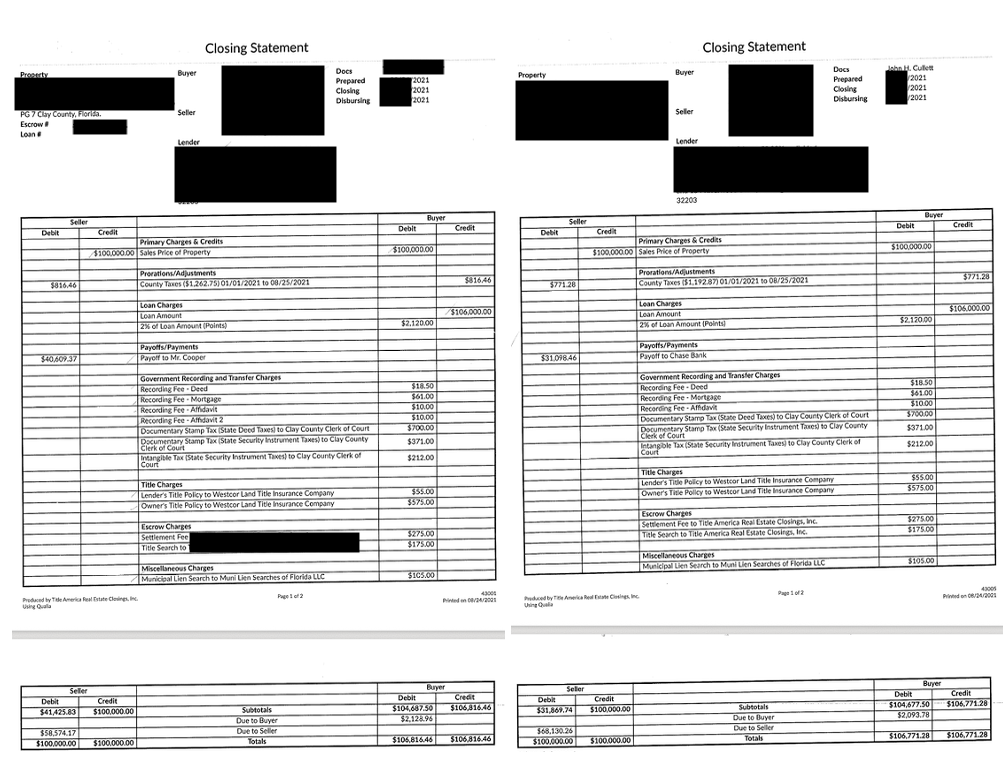

Personal information redacted. Two properties, Clay County. Both closings via Title America Real Estate Closings.

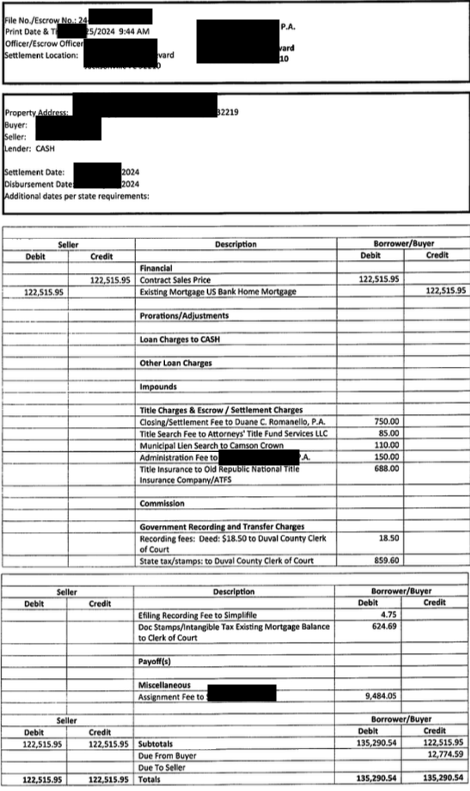

Personal information redacted. US Bank mortgage taken over. Seller brought $0 to closing. Attorney-closed.

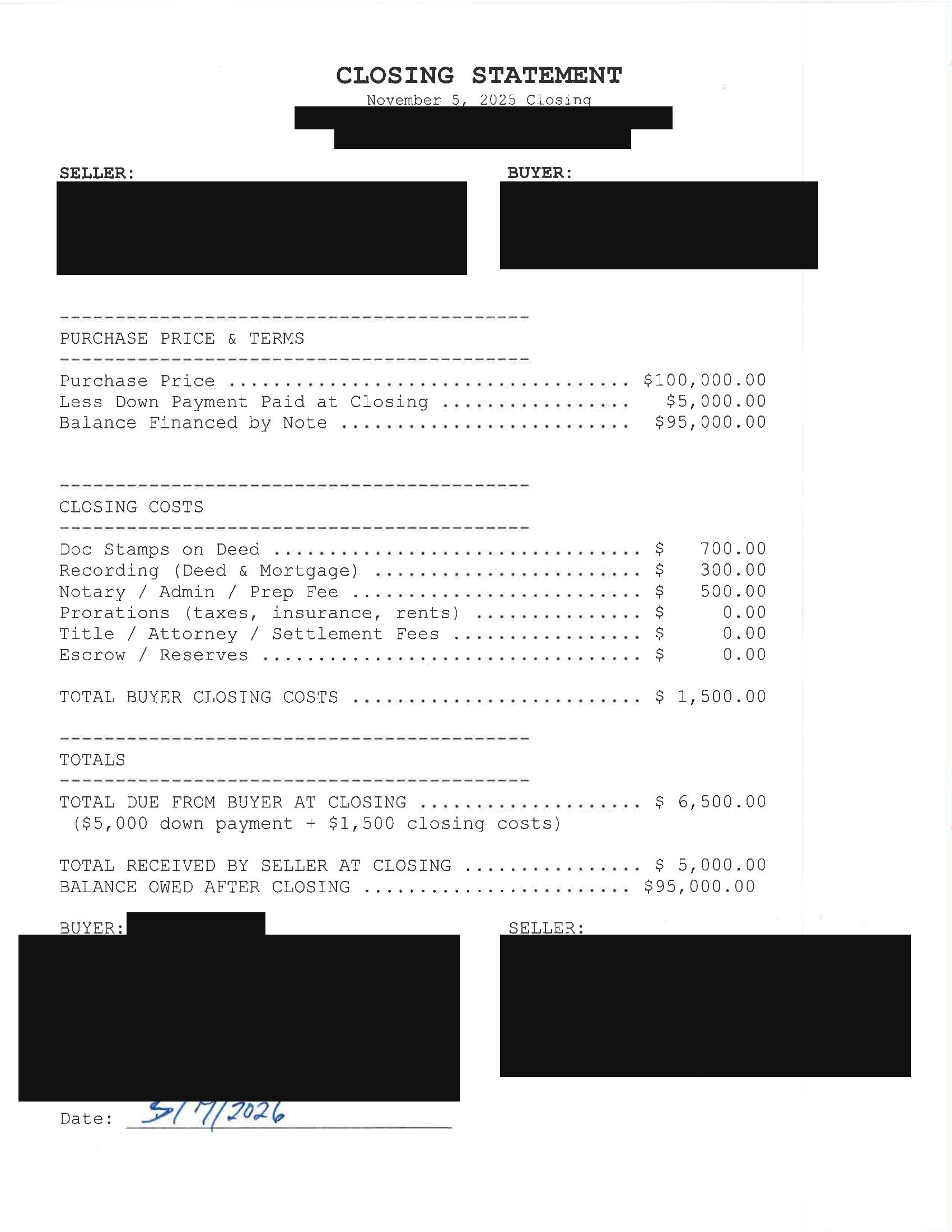

Personal information redacted. Purchase price $100,000: $5,000 down, $95,000 seller-financed at 0% interest, $500/month. Duval County. Closed directly between the two parties — no title or settlement fees.